Aluminum electrolytic capacitors sit at the heart of the electrochemical capacitor market, encompassing technologies built around aluminum, tantalum, carbon and niobium dielectrics. They remain the most cost-effective solution when a design engineer requires a combination of high capacitance and high voltage, provided that case size and environmental operating conditions are not primary constraints.

Key end-markets include consumer electronics such as computers, televisions and audio amplifiers; automotive interior systems, EV propulsion and EV charging infrastructure; and industrial applications such as motor drives, automation equipment and control systems. In terms of circuit applications, aluminum electrolytic capacitors are used almost exclusively in power supply output filters, motor start circuits and pulse discharge applications.

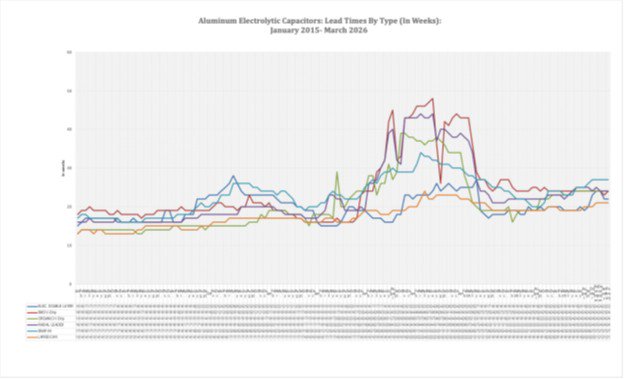

Figure 1.0

Aluminum Electrolytic Capacitor Lead Times by Type in Weeks, January 2015- May 2026 (137 Months of Data)

Source: Dennis M Zogbi, Paumanok Publications, Inc. “Monthly Market Research Report on Passive Components: May 2026”

ALUMINUM ELECTROLYTIC CAPACITORS: CURRENT MARKET CONDITIONS AND FUTURE OUTLOOK

The market for aluminum electrolytic capacitors has faced persistent headwinds from 2021 through 2026, as illustrated in the Paumanok lead-time table (Figure 1.0), which tracks all major aluminum capacitor configurations across this period. The data reveals how a convergence of supply chain disruptions has reshaped availability and pricing across the sector. Contributing factors include the lingering aftereffects of the COVID-19 pandemic, the ongoing impact of the Russia-Ukraine conflict on access to critical choke-point metals – particularly bauxite and alumina processing – and more recent geopolitical trade tensions affecting raw material flows.

At the manufacturing level, the precision electrochemical processes required to etch and form anode and cathode foils – operations that demand continuous and stable electrical energy – have been further disrupted by seismic activity in Japan and recurring power grid instability in China. These production vulnerabilities have compressed output capacity at key manufacturing nodes and extended lead times across the supply chain.

Given that aluminum electrolytic capacitors are foundational components in a broad range of high-volume end markets – including computers and servers, home theater and audio electronics, electric vehicles and EV charging infrastructure – supply chain planners and procurement teams at manufacturers serving these sectors should treat continued sourcing volatility as a baseline planning assumption through the near term.

There are seven primary configurations (or form factors) which aluminum electrolytic capacitor come in.

Radial Leaded Aluminum Capacitors

Radial leaded aluminum electrolytic capacitors remain the single largest segment of global consumption by dollar value within the aluminum electrolytic capacitor market in 2026. Their dominance is driven by broad, high-volume deployment across both consumer and professional electronics applications, where their combination of cost efficiency, reliable performance and design flexibility makes them the default choice for circuit designers.

The global market for radial leaded aluminum electrolytic capacitors is best characterized as mature – marked by slow but steady volume growth, entrenched supply relationships and limited opportunities for meaningful differentiation. Competition between Japanese and Chinese manufacturers remains intense, with Chinese vendors continuing to apply significant downward pressure on pricing through scale and vertical integration, while Japanese suppliers compete primarily on quality consistency, reliability and application engineering support. The net effect is persistent and aggressive price erosion across the segment, compressing margins for all participants.

Despite this competitive dynamic, demand remains structurally stable, underpinned by the continued production of power supplies, consumer appliances, audio equipment and industrial electronics – all of which rely heavily on radial leaded configurations. For procurement teams, this market environment offers continued pricing leverage, though supply chain diversification remains advisable given ongoing geopolitical and manufacturing risks outlined earlier in this report.

Vertical Chip Capacitors (V-Chip)

Vertical chip aluminum electrolytic capacitors represent one of the most dynamic growth segments within the broader aluminum capacitor market in 2026, having posted the strongest gains in both value and volume over the preceding five years. This sustained growth trajectory is primarily driven by robust demand from the automotive electronics sector – particularly advanced driver assistance systems (ADAS), in-cabin infotainment and EV power management – as well as continued expansion across multiple segments of the computing industry, including AI server infrastructure, edge computing and high-performance consumer devices.

A key structural driver of this growth is the ongoing displacement of radial leaded aluminum capacitors in space-constrained designs. As product form factors continue to shrink across consumer and professional electronics, vertical chip configurations offer a volumetrically efficient alternative without sacrificing capacitance or voltage performance. Core end-markets driving this substitution include thin and lightweight notebook computers, flat panel displays, gaming consoles, streaming media devices and digital imaging equipment – all of which continue to demand smaller, higher-density passive component solutions.

The vertical chip aluminum capacitor market remains highly competitive, with Japanese and Chinese manufacturers engaged in aggressive pricing rivalries that continue to compress margins across the segment. Chinese suppliers have gained considerable share through competitive pricing and expanding manufacturing capacity, while Japanese vendors maintain positioning through product quality, longevity ratings and application-specific engineering. Despite persistent price pressure, the segment retains a favorable long-term growth outlook, supported by secular demand trends in automotive electrification, AI hardware buildout and next-generation consumer electronics.

Horizontal Chip Capacitors (H-Chip)

Horizontal chip aluminum electrolytic capacitors – commonly referred to as solid polymer aluminum capacitors – are a molded chip technology built on an aluminum anode platform, designed to match the standardized case sizes of molded tantalum chip capacitors. This form factor compatibility makes them a direct functional alternative to tantalum in many design applications, and they are consequently found across many of the same end markets, including computers and servers, automotive electronics, gaming consoles and related consumer and professional devices.

Despite their technical merits, market growth for horizontal chip aluminum capacitors has been constrained by two persistent structural barriers: a price premium that has historically run approximately twice that of comparable vertical chip aluminum designs and a relatively limited vendor base that restricts supply chain flexibility and competitive pricing dynamics. Together, these factors have slowed adoption in cost-sensitive, high-volume applications where the V-chip format remains the preferred solution.

That said, the horizontal chip segment is where the majority of next-generation polymer cathode aluminum capacitor development is currently concentrated, reflecting broader industry momentum toward solid polymer electrolyte technology for its superior ESR performance, enhanced thermal stability and improved reliability under demanding operating conditions.

As manufacturing scale increases and vendor competition gradually expands, pricing is expected to become more favorable over time. Solid polymer aluminum horizontal chip capacitors are projected to capture a meaningfully larger share of the total aluminum electrolytic capacitor market over the next five years, driven by design wins in automotive electrification, AI computing infrastructure and premium consumer electronics where performance requirements justify the cost premium.

Axial Leaded Aluminum Capacitors

Axial leaded aluminum electrolytic capacitors are widely regarded as a legacy product within the global passive components market. The vendor base has contracted steadily over the years as manufacturers have shifted investment and capacity toward higher-growth form factors, and this trend has continued through 2026 with no signs of reversal.

Paradoxically, this legacy status has made the segment commercially attractive for the remaining suppliers. With a shrinking pool of qualified vendors serving a stable base of long-cycle applications, pricing power has shifted decisively toward manufacturers, allowing for healthy margins despite modest and slowly declining volumes. This dynamic is characteristic of mature legacy component segments where end-of-life design commitments and qualification costs discourage customers from switching, creating a captive and relatively price-insensitive demand base.

Primary consumption remains concentrated in the automotive industry – particularly in traditional internal combustion engine platforms and legacy vehicle electronic systems still in active production – as well as in lighting ballast applications, where axial configurations remain embedded in established designs.

Military, aerospace and certain industrial equipment segments also contribute to residual demand, as these markets frequently specify components by legacy part numbers and face significant requalification barriers. For the foreseeable future, axial leaded aluminum capacitors are expected to remain a niche but profitable product line for the small number of vendors committed to maintaining supply continuity.

Screw Terminal {Large Can}

Screw terminal large can aluminum electrolytic capacitors remain a critical component in industrial and utility-grade power electronics, with their primary application centered on inverter output filtering across a broad range of power conversion and conditioning equipment. Over the past several years, demand was propelled by rapid global expansion in renewable energy infrastructure – particularly wind turbine installations, utility-scale solar arrays and emerging wave generation systems – where these capacitors play an essential role in smoothing inverter output and ensuring grid-compatible power quality.

Beyond renewable energy, screw terminal capacitors continue to serve important roles in uninterruptible power supplies (UPS), motor drive systems, industrial automation equipment and grid-scale energy storage installations, providing a diversified demand base that extends well beyond any single end market.

Geographically, Europe had historically represented the largest regional market for screw terminal capacitor consumption, anchored by large-scale solar and wind development programs in Germany and Italy. However, by 2026, revised feed-in tariff structures introduced as part of broader regional fiscal austerity measures in both countries have materially dampened new project activity, softening near-term demand from what had previously been the segment's most dynamic regional market.

Looking ahead, growth opportunities are increasingly shifting toward North America and the Asia-Pacific region – driven by sustained renewable energy investment, grid modernization initiatives and expanding EV charging infrastructure – positioning these markets as the primary engines of screw terminal capacitor demand growth through the remainder of the decade.

Snap-In/Snap-Mount Aluminum Capacitors

Snap-mount aluminum electrolytic capacitors are characterized by their physically large form factor, high capacitance values and high voltage ratings, making them purpose-built for demanding power electronics applications. Their primary deployment is in the output filters of power supplies across industrial, commercial and professional electronics platforms, where stable, high-capacity energy storage and filtering performance are non-negotiable design requirements.

From a mounting and assembly standpoint, snap-mount configurations offer a practical and cost-effective advantage over older screw terminal designs, providing secure mechanical retention during board assembly without the additional hardware and labor associated with screw-based mounting. This ease of installation has accelerated the ongoing displacement of screw terminal products in applications where board-mounted solutions are feasible, and that transition continues through 2026.

While surface mount technology (SMT) designs have made incremental inroads across the broader capacitor market, snap-mount aluminum capacitors remain largely insulated from meaningful SMT encroachment. Their large physical size, high energy storage requirements and application-specific performance characteristics simply cannot be replicated at the capacitance and voltage levels required by competing SMT solutions available today. This technical barrier provides a degree of structural protection that few other capacitor form factors enjoy.

Looking ahead, snap-mount aluminum electrolytic capacitors are expected to maintain a stable and important role in the power electronics market through the remainder of the decade, supported by sustained demand from industrial power supplies, renewable energy inverters, motor drive systems and EV charging infrastructure – all sectors where their unique combination of high capacitance, high voltage tolerance and robust mechanical mounting continues to be highly valued.

Specialty Aluminum Capacitors

Specialty aluminum electrolytic capacitors encompass a distinct and technically demanding segment of the broader aluminum capacitor market, defined by application-specific performance requirements that standard commercial designs cannot meet. This category includes flash and pulse discharge capacitors engineered for medical device applications – such as cardiac defibrillators, surgical imaging systems and therapeutic energy delivery equipment – where precise, repeatable high-energy discharge performance is critical to patient safety and device efficacy.

Also included within this segment are capacitors manufactured in compliance with specific military and defense specifications, which demand rigorous qualification standards, extended operational lifespans and documented traceability across the supply chain. These components are designed to perform reliably under the extreme environmental and operational stresses associated with aerospace, defense electronics and mission-critical government systems.

Rounding out the specialty segment are high-temperature and high-vibration resistant aluminum capacitors, engineered for deployment in environments that would rapidly degrade standard commercial components. Key application areas include under-hood automotive electronics, industrial motor controls, oil and gas exploration equipment and aerospace platforms – all of which subject passive components to sustained thermal stress, mechanical shock and vibration profiles well beyond standard operating parameters.

In 2026, the specialty aluminum capacitor segment continues to command significant price premiums relative to commercial-grade alternatives, reflecting the elevated engineering, testing and qualification costs associated with these products. Despite relatively modest volumes compared to mainstream form factors, the segment remains highly profitable and strategically important for the small number of manufacturers with the technical capability and certifications required to serve these markets competitively.

RISING PRODUCTION COSTS FOR ALUMINUM ELECTROLYTIC CAPACITORS

Two fundamental technical principles govern the economics of capacitor production across all dielectric technologies. First, capacitance is a required functional element in virtually every electronic circuit. Second, capacitance is directly proportional to the available surface area of the finished component – meaning that the physical size and quality of raw materials used in manufacturing are central determinants of cost, pricing and the pace of technical advancement.

For aluminum electrolytic capacitors specifically, the variable cost structure is shaped by a defined set of core materials and subcomponents. The most significant cost drivers are the etched anode and cathode foils, which undergo a precision electrochemical process to maximize effective surface area and dielectric performance. The capacitor can, tabs and packaging materials represent the second major cost element, contributing both to unit economics and to the mechanical and environmental protection of the finished component. The electrolyte formulation constitutes the third primary variable cost input, playing a critical role in determining capacitance stability, ESR characteristics and operational temperature range.

Secondary, but nonetheless important, cost inputs include rubber stoppers and end-seals, which are essential for maintaining hermeticity and preventing electrolyte evaporation over the component's service life; capacitor separator papers, which isolate the anode and cathode foils within the capacitor winding; and lead wires, which provide the electrical termination interface between the component and the circuit board. Together, these six material categories define the core variable cost structure for aluminum electrolytic capacitor manufacturing and represent the primary areas of focus for cost reduction and supply chain risk management.

COST ECONOMICS AND COMPETITIVE POSITIONING OF ALUMINUM ELECTROLYTIC CAPACITORS IN 2026

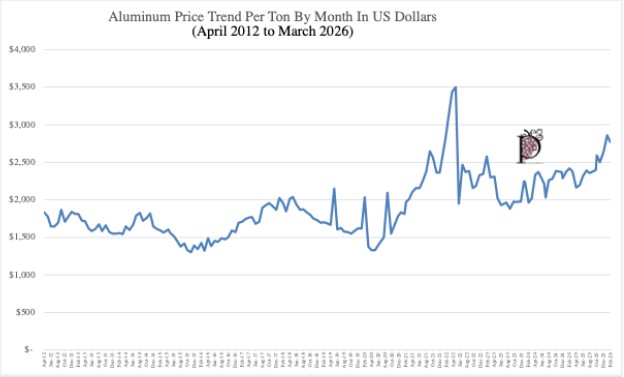

Aluminum electrolytic capacitors maintain a competitive cost structure relative to other capacitor dielectric technologies, underpinned by two enduring economic advantages: the comparatively low cost per pound of thin aluminum foil – derived from bauxite, one of the world's most abundantly sourced minerals – and the high degree of manufacturing automation that characterizes modern aluminum capacitor production. These factors deliver a favorable cost-per-microfarad ratio that few competing technologies can match at scale. Table 2.0 below illustrates the price for aluminum ore from April 2012 to May 2026. The reader should note the steady rise in aluminum feedstock over the past 12 months.

Figure 2.0

Aluminum Electrolytic Capacitor Lead Times by Type in Weeks, January 2015 - May 2026 (169 Months of Data)

Source: Dennis M Zogbi, Paumanok Publications, Inc. “Monthly Market Research Report on Passive Components: May 2026”

The Downstream Signal: Price Increases Are Already Moving Through the Chain

The cost pressures described above are no longer theoretical. They are transmitting into finished component pricing. The aluminum capacitor supply chain is now experiencing price adjustments following earlier increases for tantalum capacitors and inductors, with upstream raw material prices – metals in particular – continuing to climb toward critical cost thresholds for suppliers

That said, aluminum electrolytic capacitors carry a notably complex raw material profile relative to most other dielectric technologies. The finished component requires the integration of multiple distinct material categories – etched anode and cathode foils, separator papers, liquid or solid electrolyte, tabs, cans, lead wires, rubber stoppers and end-seals – each sourced from separate supply chains and requiring specialized manufacturing disciplines. Among all capacitor dielectrics, only polypropylene film capacitors approach a comparable level of raw material and process complexity. This complexity introduces supply chain risk and cost variability that simpler dielectric technologies do not face to the same degree.

Despite these nuances, aluminum electrolytic capacitors remain the most economical design choice available to engineers working at higher voltages and higher capacitance values in 2026. No competing dielectric technology currently offers a comparable combination of high capacitance, high voltage performance and cost efficiency – a position that is expected to hold through the foreseeable future as demand for power electronics, renewable energy systems, EV infrastructure and AI computing hardware continues to expand.

MARKET OUTLOOK AND BEYOND: AUTOMOTIVE ELECTRONICS, RENDERED ECONOMIES AND RISING INPUT COSTS FOR ALUMINUM CAPACITORS IN 2026

Automotive electronics continues to be one of the brightest demand drivers for aluminum electrolytic capacitors in 2026 and has emerged as a strategically important segment for both tactical procurement planning and long-term investment positioning. Solid polymer aluminum capacitor designs are particularly favored for EV propulsion applications – including onboard chargers, inverters, DC-DC converters and battery management systems – reflecting the broader industry preference for solid-state solutions across EV power rail architectures. Large can and snap-mount aluminum capacitors also play a critical role in DC link conversion stages, where their high capacitance and voltage handling capabilities are essential to stable power conversion performance.

From a market structure standpoint, we continue to regard aluminum electrolytic capacitors as one of the key "rendered" economies in the high-technology supply chain. The term reflects a product that is simultaneously ubiquitous, technically complex to manufacture, and deeply embedded in platform architectures that cannot easily substitute alternative solutions. Aluminum electrolytic capacitors are found in virtually every AC line-powered device – televisions, stereos, computers, home appliances and chargers – where they serve as the primary output filter on power supplies.

Their construction integrates multiple distinct disciplines: electrochemistry governs the combined anode, cathode, paper and electrolyte system, while precision tooling and machining are required to produce aluminum cans in ultra-small sizes with thick-walled structural integrity. The scale of production required to satisfy global demand – historically exceeding 100 billion pieces annually, with volumes continuing to grow – reinforces the rendered nature of this market and creates formidable barriers to entry.

Critically, input cost pressures have intensified considerably entering 2026. The aluminum capacitor supply chain is now experiencing further price adjustments following earlier increases for tantalum capacitors and inductors with Taiwanese manufacturers reporting that upstream raw material prices – metals in particular – are climbing toward critical cost thresholds for suppliers. In the United States, the aluminum foil price index rose in both Q4 2025 and Q1 2026, driven by escalating production costs tied to rising industrial electricity prices and broader inflationary pressures.

CONCLUSION

The aluminum electrolytic capacitor market in 2026 stands at a critical inflection point, shaped by the convergence of multiple structural, geopolitical and economic forces that are simultaneously redefining supply chain economics, component pricing and technology investment priorities. From the bauxite mines of Guinea to the precision electrochemical foil processing facilities of China and Japan, every stage of the aluminum capacitor value chain is experiencing measurable cost pressure, supply concentration risk and demand-side transformation.

Automotive electrification, AI computing infrastructure, renewable energy expansion and the ongoing miniaturization of consumer electronics are collectively driving robust and diversifying demand across virtually every aluminum capacitor form factor – from radial leaded and vertical chip designs to solid polymer horizontal chips, snap-mount configurations and specialty high-reliability products. At the same time, rising input costs for capacitor-grade aluminum foil, energy-intensive smelting and etching operations, U.S. tariff measures and the looming uncertainty of Guinean bauxite export controls are compressing margins and introducing a level of pricing volatility not seen in this market for nearly a decade.

For manufacturers, procurement teams and design engineers operating across the high-technology supply chain, aluminum electrolytic capacitors must now be managed not merely as a commoditized passive component but as a strategically significant material input – one whose reliable availability and stable pricing can no longer be taken for granted and whose supply chain resilience demands the same level of executive attention applied to semiconductors, rare earth materials and other acknowledged critical components of the modern electronics economy.

Dennis M. Zogbi is the author of more than 300 market research reports on the worldwide electronic components industry. Specializing in capacitors, resistors, inductors and circuit protection component markets, technologies and opportunities as well as electronic materials including tantalum, ceramics, aluminum, plastics, palladium, ruthenium, nickel, copper, barium, titanium, activated carbon and conductive polymers. Zogbi produces off-the-shelf market research reports through his wholly owned company, Paumanok Publications, Inc., as well as single-client consulting, on-site presentations and due diligence for mergers and acquisitions. He is also the majority owner of Passive Component Industry Magazine LLC.

Statements of fact and opinions expressed in posts by contributors are the responsibility of the authors alone and do not imply the opinion of the officers or the representatives of TTI, Inc. or the TTI Family of Specialists.

Follow TTI, Inc. on LinkedIn for more news and market insights.

Statements of fact and opinions expressed in posts by contributors are the responsibility of the authors alone and do not imply an opinion of the officers or the representatives of TTI, Inc. or the TTI Family of Specialists.

Follow TTI, Inc. - Europe on LinkedIn for more news and market insights.

Statements of fact and opinions expressed in posts by contributors are the responsibility of the authors alone and do not imply an opinion of the officers or the representatives of TTI, Inc. or the TTI Family of Specialists.