A day celebrated primarily in the United States, Memorial Day traditionally ushers in the beginning of school breaks, summer holidays or "rests" and beach vacations. It also brings us that much closer to the midpoint of the year, and what a year for the connector industry 2026 is shaping up to be.

Through April, bookings have increased 41.6% year to date and 47.6% year over year. Increases like this have not been seen since 2021, when the industry was recovering from the initial shock of COVID. Billings are also good, increasing 19.6% year to date and +20.9% year over year – once again reminiscent of post COVID billings.

And it isn't just one region driving this growth. Although, as the tables below indicate not all regions have performed in the same manner, they have all done remarkably well considering the regional and global headwinds the industry is currently facing.

April 2026 Connector Industry Bookings

by Region

| Region | YOY % Change | YTD % Change |

|---|---|---|

| North America | 65.8% | 53.5% |

| Europe | 33.0% | 32.7% |

| Japan | 24.1% | 20.5% |

| China | 39.6% | 39.6% |

| Asia Pacific | 64.9% | 44.0% |

| ROW | 23.3% | 31.9% |

| Total World | 47.6% | 41.6% |

April 2026 Connector Industry Billings

by Region

| Region | YOY % Change | YTD % Change |

|---|---|---|

| North America | 23.4% | 19.4% |

| Europe | 14.5% | 15.7% |

| Japan | 1.7% | 3.7% |

| China | 26.0% | 20.3% |

| Asia Pacific | 26.3% | 35.9% |

| ROW | 21.2% | 13.7% |

| Total World | 20.9% | 19.6% |

With bookings and billings like these, it is not surprising that the industry is presently sitting with approximately 14.1 weeks of backlog – a week and a half more than we ended 2025 with, as shown in the table below.

Industry Backlog

| Metric | Full Year 2025 | Apr 2026 |

|---|---|---|

| BtB Ratio | 1.00 | 1.24 |

| Beginning Backlog | $21,287 | $24,067 |

| YTD Bookings | $101,868 | $43,717 |

| YTD Billings | $99,165 | $36,191 |

| Ending Backlog | $24,067 | $31,593 |

| Backlog in Weeks | 12.6 | 14.1 |

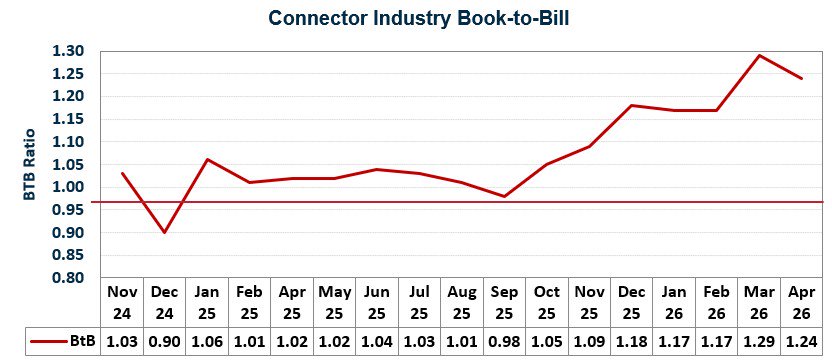

Driving this backlog is an unusually strong book-to-bill ratio. As the chart below shows, the industry has now recorded a book-to-bill ratio of over 1.0 in 20 of the last 24 (two years) months. And what makes this even more unique is that even after post COVID, when we were achieving growth over 1.0 for months on end, the growth was never beyond 1.20, as it has been in the last two months!

Naturally, growth like this has also made many industry experts and analysts concerned that a downturn is imminent. In fact, as pointed out in May 2026 by the World Economic Forum, "Nearly nine in ten chief economists surveyed expect global growth to weaken over the coming year" and "94% expect global inflation to rise as the closure of the Strait of Hormuz drives up energy and food costs and disrupts supply chains." They also noted that "92% expect greater AI adoption over the coming year, but optimism about the speed of productivity impact across industries has cooled."

Although most would agree that from an economic standpoint, the world we live in today is much different than the one we lived in five years ago and beyond, there are still several similarities, including ongoing inflation, elevated interest rates, questionable trade policies and high consumer debt. This is in addition to a slew of geopolitical uncertainties. And, because of this it is important to look at past headwinds and how they affected the connector industry in hope that we can reduce the possible pain inflicted on the industry. In the table below, past headwinds are listed and their effect on the connector industry.

Economic Downturns in the Connector Industry

Year - % Change - Reason

| Time Period | % Change in Sales | Primary Reason(s) |

|---|---|---|

| 2001 | -18.8% | Burst of the Dot-com Bubble |

| 2002 | -6.8% | Burst of the Dot-com Bubble |

| 2009 | -21.8% | Collapse of the US Housing Bubble/Financial |

| 2012 | -2.7% | European Sovereign Debt Crisis |

| 2015 | -6.1% | Crash of Chinese Stock Market/Global Oil/Strong Dollar |

| 2019 | -3.8% | Repo Market Disruption - Sharp Spike in Short-Term Interest Rates |

| 2020 | -2.2% | COVID-19 shutdowns |

Preceding all these downturns was generally a burst in economic activity, like what is occurring right now within the AI world. In fact, this has prompted some to compare the connector industry's growth of today with the dot-com craze that occurred in early 2000. But, rather than seeing vast amounts of money being pumped into the stock market as in 2001 and 2002, vast amounts of money are being pumped into physical things like data centers and semiconductor manufacturing facilities all in an effort to support AI.

Unfortunately, the revenues anticipated by AI have yet to come to fruition causing many to voice concerns that we are possibly overbuilding and opening financial institutions and investors to significant losses. This also implies that those involved in the manufacturing of data centers and the individual equipment to support these centers, such as servers and storage devices, may be overordering components such as connectors to ensure product delivery. For this reason, Bishop & Associates is watching connector demand closely and will continue to report on this topic.

As you prepare to enjoy the upcoming summer months, remember that for the most up-to-date and valuable information on the global connector industry, subscribe to the Bishop Report, the connector industry's most comprehensive source of information and analysis on connector companies, market sectors, products and trends. For information on how to order the Bishop Report, click here.

Follow TTI, Inc. on LinkedIn for more news and market insights.

Statements of fact and opinions expressed in posts by contributors are the responsibility of the authors alone and do not imply an opinion of the officers or the representatives of TTI, Inc. or the TTI Family of Specialists.

Follow TTI, Inc. - Europe on LinkedIn for more news and market insights.

Statements of fact and opinions expressed in posts by contributors are the responsibility of the authors alone and do not imply an opinion of the officers or the representatives of TTI, Inc. or the TTI Family of Specialists.