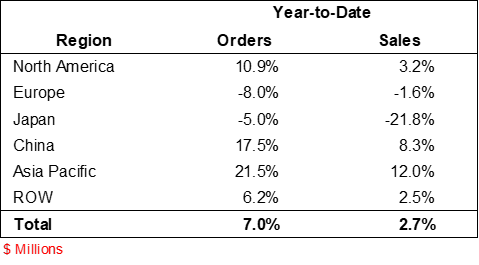

Although not what would be called exciting, business in the first half of 2024 was positive. Through June of 2024, orders are up 7.0% and sales are up 2.7%.

While the worldwide connector industry ended the first half with orders and sales growth, results are mixed by geographic region as the following table shows.

Orders and Sales

First Half 2024

Percentage Change to Prior Year

Growth is coming from North America, China and the Asia Pacific region. Europe is struggling right now with slowing GDP and unemployment at 6.5%. Japan’s GDP is also slowing, and the value of the dollar, which is how Bishop tracks sales, has been increasingly strong, drastically weaking the value of the yen. As the value of the yen improves (the yen has gained 10% over the dollar this past month), this should improve.

Anticipated Performance of Second Half of 2024 and a Look at 2025

Historically, the second half of the year is better than the first half. In fact, over the past decade, the first half of the year accounts for 48.9% of full year sales and the second half 51.1%.

The industry shipped $42,263 million through June 2024. Using this historical forecasting method, the industry will ship $86,427 million in 2024. This is a 5.6% growth over 2023 results of $81,854 million.

The Bishop forecast is slightly higher, projecting full year growth of 5.8%. We base this forecast on several things, one being the positive trend in orders, specifically the book-to-bill ratio that was 1.05 and 1.09 in May and June respectively.

Additionally, order growth has been very encouraging over the past three months, with April bookings up 10.7%, May up +.3% and June up 10.7%.

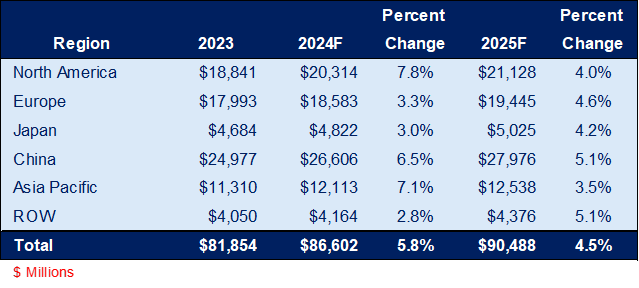

Bishop’s full year 2024 and 2025 forecast is shown in the following table.

2023, 2024 and 2025

Industry Sales Forecast

by Geographic Region

with Percent Change

The industry has achieved a compound annual growth rate (CAGR) of 5.0% since the beginning of the 21st century. You will note that our 2024 and 2025 forecast is at the historical norm. We do not see anything on the horizon for the next six months that would encourage us to forecast double-digit growth.

Conversely, there are some serious headwinds that are not positive for future business conditions.

- Inflation continues to be a key issue worldwide, although there are recent signs that inflation is slowing.

- Unemployment is increasing in the United States and Europe.

- GDP is slowing worldwide, particularly in Europe.

- Cyberattacks are becoming more frequent and more severe, creating havoc not only in an individual country but also worldwide as seen by the recent IT attacks on the global airline and banking industry. It is important to remember that a cyberattack on the financial sector can pose a serious threat to global financial security.

- Geopolitical issues such as Russia/Ukraine, Israel/Hamas/Iran and China’s pressure on Taiwan.

- Mortgage rates are high as are auto loans and credit card rates, coupled with dwindling savings.

All these headwinds reinforce the fact Bishop only anticipates modest growth over the next year and a half.

First Half 2024 Analysis by Industry Segment

The following is what we are recording and hearing from the industry’s leadership.

Automotive: This is the largest market for connectors. Connector sales in this space are flat to down single digits. Demand for automotive connectors is particularly challenging in Europe.

Transportation: Trucks, buses, rail and commercial air. Demand is slow, much like the automotive market. The number of quality issues that have plagued the commercial air business has also placed a significant damper on business.

Industrial: Sales through the first half are down double digits. Organically, TE reported -24% in the second quarter 2024 and Amphenol -5%.

Information Technology and Data Devices: Note, this segment covers aspects of both the computer and peripheral and telecom sectors within Bishop. Sales are up high double digits caused by the boom in artificial intelligence (AI). TE and Amphenol report organic sales up 32% and 56% respectively in calendar year 2Q 2024. High-speed PCB connector types and high-speed cable assemblies are in demand.

Medical is up mid single digits.

Military/Aerospace (Defense): Sales are up in the high single/low double digits. Amphenol, the largest connector manufacturer in this segment was up 10% organically in 2Q 2024, driven primarily by today's highly dynamic geopolitical environment that is driving countries around the world to expand their investment in both current and next-generation defense technologies.

Connector Pricing and Lead Times

If there is anything good about inflation it is that it makes it more difficult for OEMs/end-use equipment manufacturers to demand price concessions. Feedback from the industry is that there is no serious pressure to reduce connector prices. In fact, on selected products, mainly in the IT/data market, modest price increases are being implemented with little to no backlash. In general, Bishop classifies 2024 connector prices year-to-date as stable.

The same can be said about lead times. According to the OEMs and end-use equipment manufacturers we have spoken with, lead times appear to be at acceptable levels, with no long-term delays expected for the balance of the year.

Statistical Second Half Industry Performance

Statistically, Bishop is guardedly optimistic and believe the second half will be better than the first half. The following is how we see connector demand by quarter:

Connector Sales by Quarter

2022, 2023 and 2024

Factors driving Bishop’s 2024 forecast by quarter.

- Orders are improving and the backlog is up $1.0 billion over 2023-year end.

- Connector prices are stable.

- Inflation appears to be slowing.

- Artificial intelligence (AI) is booming.

- Automotive is a concern.

- Europe is a concern.

- Geopolitical issues are a concern.

Bishop & Associates, incorporated in 1985, is the leading research firm on the connector industry. The Bishop Report is a monthly newsletter that tracks the performance of the industry. To learn more or to subscribe, follow this link.

Follow TTI, Inc. on LinkedIn for more news and market insights.

Statements of fact and opinions expressed in posts by contributors are the responsibility of the authors alone and do not imply an opinion of the officers or the representatives of TTI, Inc. or the TTI Family of Specialists.

Follow TTI, Inc. - Europe on LinkedIn for more news and market insights.

Statements of fact and opinions expressed in posts by contributors are the responsibility of the authors alone and do not imply an opinion of the officers or the representatives of TTI, Inc. or the TTI Family of Specialists.