All 14 primary electronic metals are seeing price increases in the March 2026 quarter. However, some metals have experienced particularly sharp volatility – most notably ruthenium, which is used in thick film inks, chip resistors and networks.

Resistors represent one of the largest sources of worldwide ruthenium consumption. The metal is used primarily in thick film resistive pastes, where it is a critical functional ingredient in the manufacture of chip resistors and resistor networks found in virtually every electronic device.

Beyond resistors, ruthenium serves additional industrial roles: it functions as a cracking catalyst in the petrochemical industry, is applied as a protective and performance-enhancing coating in hard disk drives and appears as a component in a range of specialized and esoteric chemical compounds.

Because resistor manufacturing accounts for such a dominant share of ruthenium demand, the metal's price is highly sensitive to any shifts in resistor supply and demand dynamics. A slowdown in electronics production, a change in resistor technology or a surge in consumer electronics output can each have an outsized and rapid effect on ruthenium pricing – making it one of the more reactive and closely watched of the electronic metals.

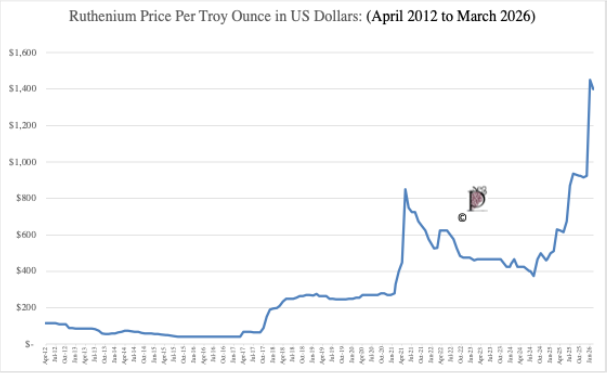

Ruthenium has experienced a dramatic price increase, rising from $40 per troy ounce to as high as $1,400 per troy ounce – a staggering 35-fold increase. This surge corresponds closely with broader disruptions in the supply of platinum group metals (PGMs) and understanding why requires examining ruthenium's unique position in the mining ecosystem.

Ruthenium is not mined directly but is instead recovered as a byproduct of platinum mining, primarily from operations in South Africa and, to a lesser extent, Russia and Zimbabwe. This means its supply is entirely dependent on the fortunes of the platinum industry rather than its own demand fundamentals. Several factors can disrupt this supply chain:

- Mining output reductions: Any curtailment of platinum mining activity, whether due to labor strikes, rising production costs, mine closures or falling platinum prices making mining less economically viable, will directly reduce the availability of ruthenium as a co-product, regardless of how strong ruthenium demand may be.

- Geopolitical risk: With primary PGM production heavily concentrated in South Africa and Russia, political instability, sanctions or trade restrictions in either country can sharply constrain the global ruthenium supply almost overnight.

- Refining and processing bottlenecks: Ruthenium is extracted during the complex refining of PGM ore. Any disruption to refinery capacity or processing infrastructure limits how much ruthenium can be separated and brought to market.

- Low inventory buffers: Because ruthenium is a byproduct metal with historically low prices, producers and consumers have typically maintained minimal strategic stockpiles, meaning any supply shock is quickly felt in the spot market with little buffer to absorb the disruption.

- Inelastic supply response: Unlike primary metals, ruthenium supply cannot be increased independently. Even at $1,400 per troy ounce, miners cannot simply produce more ruthenium without first increasing platinum output, making the supply response slow and constrained.

Together, these factors make ruthenium's price uniquely vulnerable to external shocks and help explain why disruptions in the broader PGM market can trigger such extreme price volatility in this relatively obscure but industrially critical metal.

Figure 1. Ruthenium Price per Troy Ounce in US Dollars by Month, April 2012 to March 2026

Source: Paumanok Publications, Inc. Industrial Market Research – Monthly Market Research Report on Passive Components and Raw Materials. Paumanok has red flagged this price increase for Ruthenium metal because of its significant impact on the cost to produce thick film chip resistors.

Seeking Alternative Metals

The sharp rise in ruthenium prices has prompted many customers to explore alternative resistor designs – specifically thin film resistors using nickel rather than ruthenium-based thick film pastes. However, this shift comes with a significant practical constraint: the manufacturing economies of scale achievable with thin film nickel resistors are only a fraction of those possible with thick film chip resistors, which rank among the highest-volume components produced anywhere in the world, with output measured in the trillions of pieces annually.

As we have noted, the thick film chip resistor market represents one of the most precarious supply chains in the electronics industry. Its vulnerability stems from two structural realities. First, the product is "rendered" in nature, meaning its core functional material, ruthenium, is consumed and cannot be recovered or recycled from finished resistors at any meaningful scale. Second, the market is critically dependent on a rare precious metal that is itself a byproduct of an entirely separate industry. Because ruthenium supply is governed by the economics of platinum mining rather than resistor demand, the thick film chip resistor industry is effectively subject to supply forces entirely outside of its own control, a rare and uncomfortable position for a component so fundamental to modern electronics.

How Thick Film Chip Resistors Are Made

Thick film chip resistors begin with an alumina ceramic substrate – typically 96% purity alumina – a remarkably durable material that is laser-trimmed to form the precise rectangular chip shape and to achieve the desired ohmic value.

The resistive element is created by screen-printing a ruthenium oxide paste onto this substrate. This paste is produced by combining ruthenium precious metal with an inorganic binder to form a functional ink. Once printed, the resistive layer is dried under low heat and then fired at high temperature, permanently bonding it to the alumina substrate.

The final stage is termination, the process by which the chip is made solderable and ready for board mounting. This is achieved through a bulk dipping and plating process in which the chip's end-caps are metallized with a silver-bearing termination paste, followed by the application of a nickel barrier layer and a lead solder coating, allowing the finished component to be reliably soldered onto a printed circuit board.

How Thick Film Resistor Networks Are Made

A thick film resistor network combines two or more resistive elements on a single insulating substrate. They are typically used where a circuit requires between four and 36 low-value resistors, as packaging multiple resistors into a single component saves valuable printed circuit board (PCB) space. Commercial networks are available in two primary package formats: dual-in-line (DIP) packages, which are traditionally molded in plastic and the larger single-in-line (SIP) packages, which are predominantly conformal-coated designs manufactured in Asia.

The substrate used in resistor networks is predominantly 96% purity alumina ceramic – the same highly durable material used in chip resistors. Conductive interconnections are formed by screen-printing a precious metal powder suspended in a volatile binder to create a conductive ink or paste. Once fired, this composition forms a solid, low-resistance pathway for electrical current.

A resistive ink, predominantly a ruthenium cermet composition mixed with powdered glass frit and a volatile binder, is then screen-printed over the ends of the conductors and fired to produce a hard, stable resistive element. A laser is then used to trim each resistive element to its precise target value. Standard configurations typically range from 10 milliohms to 10 ohms, with tolerance ratings of ±2%. One notable design limitation is power handling: each individual deposited resistor is rated at less than ½ watt, constraining the amount of heat dissipation the network can manage.

The completed assembly is packaged either as a plastic-molded DIP or a conformal-coated SIP. Variations on this basic format include the thick film R/C network, which integrates both resistors and capacitors on a single substrate and specialty flatpack designs that can accommodate as many as 50 resistors per package.

Resistor networks have a long history. Industry leaders began packaging individual resistors into network configurations as far back as 1963, making them one of the earliest examples of component integration designed to reduce pick-and-place assembly costs and maximize PCB real estate. Today, however, both primary formats face competitive pressure: the SIP market is increasingly challenged by thick film resistor chip arrays, while the DIP market faces encroachment from thin film integrated passive devices.

Resistor chip arrays have been a viable packaging alternative for some 30 years. By mounting two, three, four or even eight resistors on a single bridge structure, chip arrays allow multiple resistors to be placed on a board simultaneously, offering PCB manufacturers a meaningful reduction in assembly time and insertion costs.

Raw Material Costs: The Primary Risk Factor in Thick Film Chip Resistor Production

Among all the cost inputs in thick film chip resistor manufacturing, raw materials represent the single largest variable cost. While overhead and labor also contribute, it is the price and availability of key metals that have historically driven the most significant cost swings over the past three decades. This exposure is not limited to ruthenium alone. The ceramic alumina substrate is also subject to price and supply variability. Together, these two materials form the core of the industry's cost risk, capable of either squeezing manufacturer profitability or forcing price increases onto customers with relatively little warning.

Thick Film Chip Resistor Lead Times React

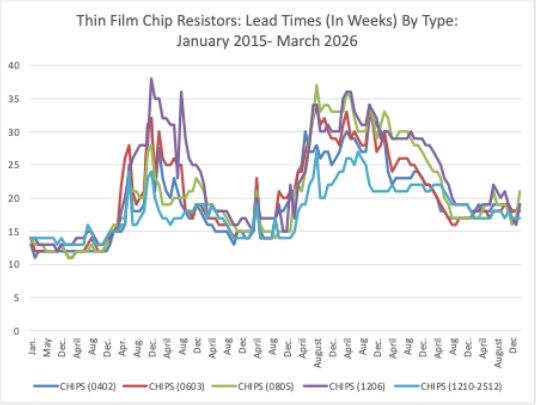

Thick film chip resistors showed a large-scale increase in lead times from February to March 2026 which affected all EIA case size chips from 0201 to 1206 (see Figure 2). We believe this to be a response to the price increase in ruthenium in the same time period.

Figure 2. Global Thick Film Chip Resistor Lead Times by Month, January 2013 to March 2026

Source: Paumanok Publications, Inc. Industrial Market Research – Monthly Market Research Report on Passive Components and Raw Materials. Lead times are jumping each time there is a major increase in the price of ruthenium metal.

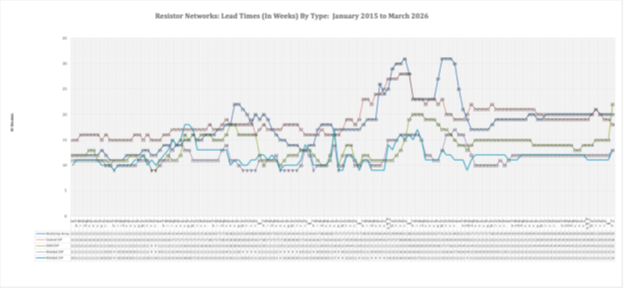

Thick Film Resistor Network Lead Times Also React

The legacy resistor network market is different from other passive component product markets we analyze. Some of these product lines can be scarce and it’s reflected in lead times, especially for the coated-SIP design. Other product markets reflect the steady state of the industry and the limited number of brand name vendors in the segment. The networks are also large volume consumers of ruthenium metal because of their size. They are also coated with additional metal interconnects between individual components in the bridge.

The February to March 2026 data supports this market for resistor networks as increasing for high-voltage applications in computing, industrial and infrastructure related components.

Figure 3. Resistor Networks: Lead Time Trends by Type (Array, SIP and DIP)

Source: Paumanok Publications, Inc. Industrial Market Research – Monthly Market Research Report on Passive Components and Raw Materials. Lead times are jumping each time there is a major increase in the price of ruthenium metal.

Ruthenium Dependency: The Risk Factor You Can't Ignore

Thick film chip resistors are the true workhorse of the electronics industry. Inexpensive and virtually ubiquitous, they are consumed in the trillions of pieces each year because every electronic circuit requires precise ohmic values to function, and thick film chip resistors deliver those values in an ultra-compact package combining ceramic, glass, ruthenium and silver. Among all electronic components, only ceramic chip capacitors rival them in terms of sheer production and consumption volume.

Their presence spans virtually every electronic circuit in the world. Major application areas include wireless handsets, computer motherboards, hard disk drives, monitors, automotive electronic subassemblies, televisions, stereo amplifiers and industrial electronics – essentially any device with a circuit board.

It is precisely these massive economies of scale, combined with their low unit price and the high concentration of manufacturing among a small number of producers, that make thick film chip resistors among the most operationally challenging electronic components to produce and supply reliably. Their deep structural dependence on the platinum group metals supply chain – through their long-standing reliance on ruthenium – introduces a significant and difficult-to-manage cost pressure. As ruthenium prices remain volatile, this exposure is emerging as one of the most consequential risk factors facing the broader high-tech economy in the coming fiscal year.

Variable Raw Material Costs

The variable cost associated with raw materials makes passive components somewhat unique because the supply chain must rely in whole or in part upon outside merchant market vendors and engineered materials processors to supply the engineered powders and pastes to produce their passive electronic components.

Historically, changes in metal prices and availability have proven to be the greatest risk factors in the cost to produce both mass produced capacitors and resistors – each in the trillions of pieces. In recent months, the price of ruthenium has reached levels that have not been seen for years.

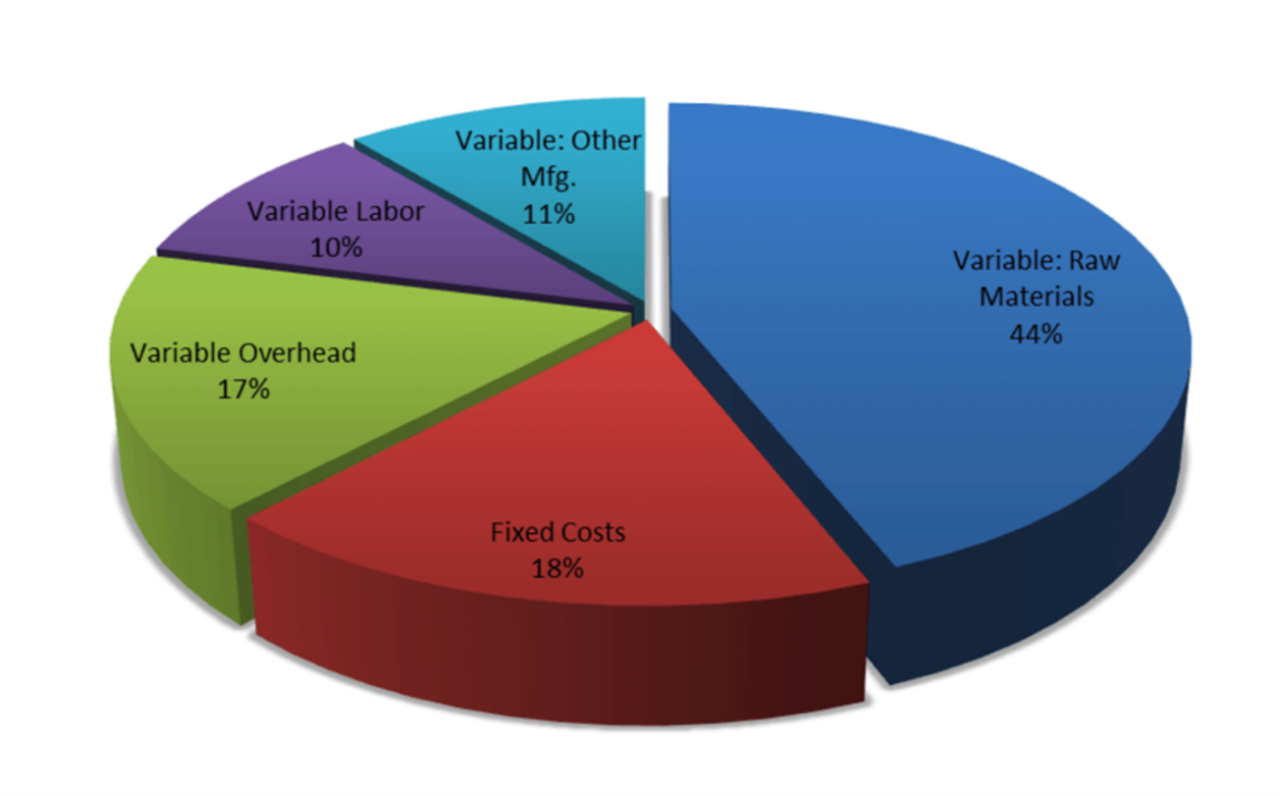

Variable raw material costs average 44% of the costs to produce for the worldwide resistor industry. Any substantial price increase in feedstock metals consumed here will have an eventual impact on thick film chip resistor pricing and availability (see Figure 4).

Figure 3. Fixed and Variable Costs to Produce Thick Film Chip, Network and Array Resistors

Source: Paumanok Publications, Inc. Variable Raw Material Costs Include Substrates, Resistive pastes, Terminations, Additives, Epoxies and Electronic Glass

Summary and Conclusion

Unprecedented increases in the price of ruthenium, a key element in the production of thick film pastes used in thick film chip resistors, has resulted in extended lead times for the ubiquitous resistor component. Because of the large percentage of variable costs in the production of chip resistors relying on raw materials, expect price increases. The reasons for these price increases can be traced directly to disruptions in platinum mines. Ruthenium is a by-product of platinum mining. Platinum has a primary use as an autocatalyst, and that market is losing ground to electric vehicles that require no catalytic converter.

This price volatility has caused customers to seek alternative resistor designs also based upon thin film nickel. Unfortunately, the economies of scale in manufacturing for thin film resistors are but a small fraction of that of thick film chips, one of the largest volume products produced in the world (measured in the trillions of pieces). Resistors represent a significant volume of worldwide consumption for ruthenium metal (with additional uses as a cracking catalyst, a hard disc drive coating and as an esoteric chemical compound). Therefore, the metal is very sensitive to any changes in resistor supply and demand the global high-tech economy and its signpost on the current market conditions should not be overlooked by the precious metal market analyst.

Outlook

For thick-film resistor manufacturers using ruthenium-based inks and chip resistor producers, this metal represents the most serious cost challenge in decades. Ruthenium's outlook depends heavily on Russian supply, which remains constrained by sanctions. South African production faces ongoing power shortages (Eskom load-shedding) and labor issues. With no substitutes offering comparable performance in precision resistor applications, manufacturers face difficult choices: (1) accept elevated costs, (2) reformulate inks with lower ruthenium loading or (3) pass costs to customers. This commodity deserves intense supply chain scrutiny and strategic inventory positioning.

Follow TTI, Inc. on LinkedIn for more news and market insights.

Statements of fact and opinions expressed in posts by contributors are the responsibility of the authors alone and do not imply an opinion of the officers or the representatives of TTI, Inc. or the TTI Family of Specialists.

Follow TTI, Inc. - Europe on LinkedIn for more news and market insights.

Statements of fact and opinions expressed in posts by contributors are the responsibility of the authors alone and do not imply an opinion of the officers or the representatives of TTI, Inc. or the TTI Family of Specialists.