How AI Infrastructure and Shifting EV Markets Are Reshaping Tantalum Capacitor Demand

EXECUTIVE SUMMARY

The tantalum capacitor market is experiencing a critical inflection point that defies conventional supply chain logic. While tantalum ore prices have surged nearly 110% from their 2024 lows—jumping from approximately $55 per pound to $115 per pound by January 2026—tantalum capacitor lead times remain surprisingly stable at 16 to 18 weeks. This represents only a modest extension from baseline levels, not the crisis conditions one would expect given such dramatic raw material cost inflation.

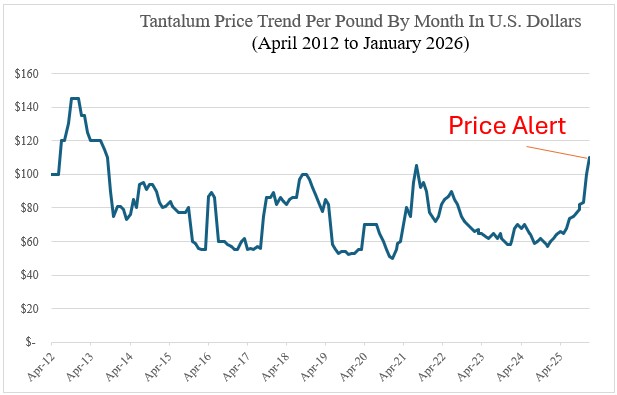

Source: Paumanok Monthly Report on Raw Materials for Passive Electronic Components January 2026 Update- Shows the estimated global price per pound for tantalum ore in U.S. dollars.165 months

This disconnect reveals three critical market dynamics:

First, supply chains have not yet transmitted raw material price shocks into finished component availability constraints. Manufacturers are absorbing cost increases rather than curtailing production, suggesting healthy profit margins and strategic positioning for market share.

Second, demand composition is undergoing fundamental structural change. The electric vehicle market—particularly in the United States—is experiencing growth deceleration after years of exponential expansion. Simultaneously, artificial intelligence infrastructure buildout has emerged as an unexpected consumption vector, with hyperscale data centers deploying tantalum capacitors at unprecedented densities.

Third, procurement organizations are increasingly concerned about capacity allocation between these competing end markets. The narrative that AI hyperscale systems are absorbing manufacturing capacity previously destined for EV applications is gaining traction, creating strategic uncertainty about future availability and pricing.

This report examines 165 months of tantalum ore pricing data and 132 months of capacitor lead time tracking to provide context for current market conditions and assess the sustainability of this unusual price-availability disconnect.

TANTALUM ORE PRICE VOLATILITY: A 165-MONTH PERSPECTIVE

Our comprehensive tracking program, spanning April 2012 through January 2026, documents one of the most strategically important and price-volatile materials in the passive electronic components industry. The current price environment—with tantalum ore approaching $115 per pound—represents the culmination of multiple structural shifts and demand transformations that have fundamentally altered market dynamics.

The 2012-2016 Correction: From Speculation to Reality

Our data series begins at a remarkable $145 per pound peak in April 2012, representing the tail end of a speculative bubble driven by conflict mineral legislation concerns. The Dodd-Frank Act's Section 1502, enacted in 2010, created unprecedented scrutiny of tantalum sourcing from the Democratic Republic of Congo and adjoining regions. Manufacturers engaged in panic buying and strategic stockpiling of certified conflict-free material, artificially inflating prices well beyond fundamental supply-demand equilibrium.

The subsequent correction was both severe and protracted. Prices declined 60% over four years, bottoming near $55 per pound in mid-2016. This extended bear market reflected converging factors: resolution of initial compliance uncertainties, increased Australian production from Talison Lithium's Greenbushes and Global Advanced Metals' Wodgina facilities and demand softness as manufacturers optimized designs toward alternative dielectrics where technically feasible.

The 2013-2014 period showed particular weakness, with prices consolidating in the $80-$90 range before breaking lower. Excess inventory liquidation across the supply chain coincided with increased secondary tantalum recovery from tin slag operations in Southeast Asia, particularly Thailand and Malaysia, creating a supply overhang that took years to absorb.

2016-2019 Stabilization: The Calm Before Multiple Storms

Following the 2016 trough, tantalum markets entered relative stability, trading predominantly in the $55-$85 range. This reflected a balanced supply-demand as speculative inventory had been purged and consumption normalized around sustainable patterns from tantalum capacitor manufacturers—Kemet, AVX, Vishay, and Murata—serving automotive, industrial and telecommunications applications.

However, significant monthly volatility persisted, with $10-$15 per pound swings occurring within quarters. These oscillations typically corresponded to temporary supply disruptions from African artisanal mining operations, where production remains highly sensitive to regional security conditions or procurement cycles among major manufacturers.

The 2018 mid-year spike to approximately $105 per pound deserves particular attention. Robust smartphone production volumes drove tantalum capacitor demand while temporary mine production shortfalls in both African and Australian operations—due to labor disputes and weather-related logistics disruptions—created supply tightness. This episode foreshadowed the volatility that would define subsequent years.

Pandemic Disruption and Recovery: 2020-2022

COVID-19's onset in early 2020 initially compressed prices as electronics manufacturing shutdowns and demand uncertainty prompted buyers to defer purchases and draw down inventories. Prices briefly tested the $55 level again in mid-2020, revisiting 2016 lows.

This compression proved remarkably transient. By late 2020, prices had recovered to the $70 range as work-from-home infrastructure buildouts and digitalization trends drove electronics demand to unprecedented levels. The 2021-2022 period demonstrated tantalum's new volatility paradigm, with prices oscillating between $65 and $110 per pound in response to supply chain disruptions, logistics constraints and erratic demand patterns.

The spring 2021 spike to approximately $110 per pound was particularly notable, driven by semiconductor shortage-related effects rippling through the entire electronics materials supply chain. Tantalum capacitor manufacturers, faced with unpredictable component demand and extended lead times, engaged in precautionary buying that temporarily tightened spot market availability.

The Current Rally: 2024-2026 Structural Tightening

Perhaps the most striking feature of our 165-month data series is the dramatic price appreciation from mid-2024 through January 2026. After trading in a relatively compressed $55-$75 range through much of 2023 and early 2024, tantalum prices have surged to approximately $115 per pound—a near-doubling from the lows and approaching levels not sustained since the 2012-2013 speculative period.

This rally reflects multiple reinforcing factors that have fundamentally tightened the supply-demand balance. On the supply side, production constraints have intensified. African artisanal mining, historically providing 30-40% of global primary tantalum supply, faces increasing regulatory pressures, formalization requirements and competing labor demands from other mining sectors. Australian hard-rock production, while more stable, has not expanded meaningfully to offset these losses, as mining companies prioritize lithium extraction over tantalum recovery from spodumene deposits.

Simultaneously, demand drivers have strengthened considerably. The electric vehicle revolution—despite recent U.S. market softness—continues driving structural demand growth globally, with modern EVs containing two to three times the tantalum capacitor content of internal combustion vehicles for power management, battery management systems, and advanced driver assistance systems. Additionally, the artificial intelligence computing boom has created unexpected demand intensity, as AI data centers require exceptionally high capacitor counts for power delivery to GPU arrays and high-performance computing systems.

TANTALUM CAPACITOR LEAD TIMES - A DECADE OF SUPPLY CHAIN TURBULENCE AND MARKET TRANSFORMATION

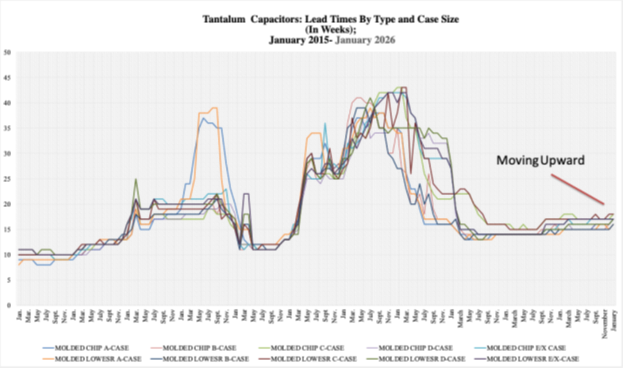

We have maintained continuous tracking of tantalum capacitor lead times across multiple package configurations for over a decade132 months, from January 2015 through January 2026. This comprehensive data set, covering both molded chip and molded LOWESR (Low Equivalent Series Resistance) configurations across A-Case through EX-Case sizes, provides unprecedented visibility into the supply chain dynamics, capacity constraints and demand volatility that have defined the tantalum capacitor market through one of its most turbulent decades in history. The purpose of this is to show the reader that demand has not yet been impacted by the increase in tantalum ore prices, but is beginning to move upward as anticipated because of tantalum capacitor consumption of tantalum ore, powder and wire and silver spray in molded chip production.

Source: Paumanok Monthly Report on Passive Electronic Components January 2026 Update- Shows the estimated global lead times for tantalum capacitors by type and case size.

TANTALUM CAPACITOR LEAD TIMES: THE DISCONNECT PARADOX

Our 132-month tracking of tantalum capacitor lead times, from January 2015 through January 2026, reveals a market dynamic that defies conventional wisdom. While tantalum ore prices have nearly doubled in the past 18 months, capacitor lead times remain remarkably stable at 16-18 weeks—elevated from baseline but far from the crisis levels of 2018 (37-40 weeks) or 2021-2023 (35-43 weeks).

This disconnect reveals critical insights about supply chain resilience, manufacturing capacity and the lag between raw material cost inflation and finished component availability constraints. More importantly, it demonstrates that demand has not yet been materially impacted by tantalum ore price increases—but early indicators suggest this stability may be temporary.

2015 Baseline: The Era of Stability

Our tracking begins in January 2015 with lead times in a remarkably stable configuration. Across all package types and configurations—molded chip and molded LOWESR in A-Case through EX-Case sizes—lead times clustered tightly in the 8–11-week range, reflecting a well-balanced supply-demand environment. The global tantalum capacitor industry had successfully navigated conflict minerals compliance transition, capacity utilization rates were healthy but not strained and end-market demand from smartphones, tablets and industrial electronics was growing at predictable, manageable rates.

The tight clustering of lead times across different case sizes during this period is particularly noteworthy. It indicates manufacturing bottlenecks were not concentrated in any specific production process, whether powder processing, anode formation or final assembly and testing. Capacity was balanced across the production chain, allowing manufacturers to maintain consistent delivery performance regardless of package configuration.

Crisis Periods: 2018 and 2021-2023 Supply Constraints

The spring and summer of 2018 witnessed the first dramatic lead time spike, with multiple configurations surging to the 35-40-week range. Molded LOWESR A-Case reached approximately 39 weeks in June-July 2018, while molded chip A-Case and B-Case configurations peaked near 37-38 weeks. This fourfold increase from baseline levels created severe supply chain disruptions across multiple electronics sectors.

The 2018 crisis was driven by smartphone production seasonal surges coinciding with accelerating automotive electronics growth. Critically, parallel MLCC market constraints drove some designers to substitute tantalum capacitors where either technology could meet specifications, further intensifying demand on already-strained capacity.

However, the 2021-2023 extended crisis dwarfed the 2018 episode in both severity and duration. From mid-2021 through mid-2022, tantalum capacitor lead times reached levels that fundamentally challenged traditional electronics supply chain management practices. Multiple configurations sustained lead times in the 35-43-week range, with peak readings showing molded LOWESR C-Case at approximately 43 weeks.

What distinguished this crisis was its duration—elevated lead times persisting for 18-24 months rather than a sharp spike followed by rapid normalization. This reflected not a temporary demand surge, but a structural supply-demand imbalance driven by semiconductor shortage cascading effects, precautionary component hoarding and genuine demand growth from electric vehicle production ramping aggressively as manufacturers committed to electrification roadmaps.

Current Conditions: The Gradual Extension of 2024-2026

The most recent data, from mid-2024 through January 2026, reveals a concerning trend labeled appropriately as 'Moving Upward.' After reaching a trough in the 13-15-week range in early to mid-2024, lead times have begun gradually extending again, reaching approximately 16-18 weeks for most configurations by January 2026.

This renewed extension occurs in a fundamentally different context than previous spikes. Rather than sudden demand shocks or supply disruptions, the current trend reflects structural demand growth outpacing incremental capacity additions. Electric vehicle production continues accelerating globally—despite U.S. market complications discussed below—with output exceeding 15 million units in 2025. The tantalum capacitor intensity per vehicle remains high and may be increasing as battery voltages rise and power electronics become more sophisticated.

Critically, the capacity response to renewed demand growth has been more measured than in previous cycles. Manufacturers, having experienced repeated boom-bust cycles, are more cautious about major capital commitments. Lead times of 16-18 weeks, while elevated, remain below panic levels that would typically trigger aggressive expansion. The industry appears to be managing to a higher equilibrium lead time rather than experiencing acute shortage.

THE AI-EV CAPACITY ALLOCATION QUESTION: EMERGING MARKET DYNAMICS

A critical narrative is emerging in procurement circles that deserves careful examination: are artificial intelligence hyperscale data centers absorbing tantalum capacitor manufacturing capacity that would otherwise serve the electric vehicle market? This question has significant strategic implications as both sectors compete for limited production resources.

The U.S. Electric Vehicle Market: From Exponential Growth to Deceleration

While global EV production continues accelerating—particularly in China and Europe—the United States market has experienced notable deceleration in 2025 and 2026. Several converging factors explain this dynamic:

Consumer adoption resistance: after early-adopter enthusiasm, mainstream consumers face range anxiety, charging infrastructure concerns and higher upfront costs despite incentives. Purchase consideration rates have plateaued in key demographic segments.

Policy uncertainty: federal tax credit program modifications and potential policy changes create hesitation among both manufacturers and consumers regarding long-term EV economics.

Infrastructure buildout lag: public charging network expansion has not kept pace with vehicle deployment needs, creating practical usage limitations that constrain adoption in suburban and rural markets.

Hybrid competition: improved hybrid electric vehicle offerings provide electrification benefits without range limitations, appealing to cautious consumers and reducing pure EV market share growth.

Manufacturing capacity reassessment: several major automotive manufacturers have announced delays or scaling back of aggressive EV production targets for U.S. facilities, citing weaker-than-projected demand and profitability concerns.

This U.S. market softness does not represent a global EV trend reversal—China produced over 9 million EVs in 2025, and European markets continue steady growth. However, it does suggest that tantalum capacitor demand previously allocated to U.S. EV production may be becoming available for reallocation to other applications.

AI Hyperscale Infrastructure: The Unexpected Demand Vector

Simultaneously, artificial intelligence infrastructure deployment has emerged as one of the most tantalum-intensive applications in modern electronics. The scale and characteristics of this demand vector were not anticipated in industry capacity planning as recently as 2022-2023.

AI data centers present unique tantalum capacitor requirements.

Exceptional power delivery stability requirements for GPU arrays. Modern AI training clusters deploy hundreds or thousands of high-performance GPUs, each requiring stable, clean power delivery with minimal voltage ripple. Tantalum capacitors' superior ESR characteristics and reliability under demanding thermal and electrical conditions make them preferred solutions for GPU power management modules.

High-density deployment creating multiplicative demand: a single AI training server may contain 50-100+ tantalum capacitors across power distribution, voltage regulation and signal conditioning applications. Hyperscale facilities deploying tens of thousands of such servers create concentrated demand measured in millions of capacitors per facility.

Reliability imperatives driving tantalum preference: AI infrastructure operators cannot tolerate power delivery failures that corrupt training runs or inference operations. The mission-critical nature of these workloads justifies premium component selection, with tantalum capacitors' proven reliability in demanding applications driving design wins over lower-cost alternatives.

Sustained buildout trajectory with minimal cyclicality: unlike consumer electronics with seasonal patterns or automotive with economic sensitivity, AI infrastructure investment appears relatively insensitive to near-term economic conditions. Major cloud providers and AI companies continue aggressive capital expenditure programs, creating sustained demand visibility.

Industry sources estimate that AI data center tantalum capacitor consumption has grown from essentially zero in 2021 to potentially eight to 12% of global production by late 2025. Projected buildout plans through 2027-2028 suggest this percentage could reach 15-18%, representing a demand scale comparable to traditional automotive electronics applications.

Capacity Allocation Dynamics: Competition and Constraints

The fundamental question facing procurement organizations is whether the U.S. EV market softness is freeing capacity that AI infrastructure can absorb, or whether AI demand growth would strain capacity regardless of EV market conditions.

Several factors complicate this analysis:

Global vs. regional dynamics: while U.S. EV production may be moderating, global EV production continues accelerating. Tantalum capacitor manufacturing is globally fungible; production capacity serves worldwide markets. U.S. EV demand softness may free capacity for U.S. AI data centers, but only if that capacity wasn't already committed to Chinese, European or other regional EV production.

Specification and qualification differences: automotive-grade tantalum capacitors undergo rigorous qualification processes and operate under demanding temperature, vibration and reliability requirements. AI data center applications, while requiring high reliability, may have different specification profiles. Manufacturers cannot instantaneously repurpose automotive-qualified production lines for data center applications without requalification.

Long-term commitment structures: automotive supply agreements typically involve multi-year commitments with volume guarantees and pricing structures. Even if near-term EV production volumes disappoint, manufacturers may maintain capacity allocation under existing contractual obligations, limiting availability for opportunistic AI infrastructure orders.

Manufacturing cycle time constraints: the gradual lead time extension we observe—16-18 weeks currently, potentially reaching 20-24 weeks by year-end 2026—suggests capacity is tightening but not yet saturated. If significant EV capacity were truly becoming available, we would expect lead time compression rather than extension.

Strategic Implications for Procurement Organizations

The intersection of rising tantalum ore prices, stable but gradually extending capacitor lead times, shifting EV market dynamics and explosive AI infrastructure growth creates a complex procurement environment. Several strategic considerations emerge:

1. The capacity allocation question requires active monitoring rather than passive assumptions. Procurement teams cannot assume the U.S. EV market softness automatically translates to tantalum capacitor availability. Global demand patterns and manufacturing allocation decisions are more complex than simple regional substitution.

2. AI infrastructure demand represents a new competitive pressure for traditional applications. Organizations serving industrial, telecommunications and consumer electronics markets may find themselves competing with hyperscale data center operators who demonstrate greater price insensitivity and longer commitment horizons.

3. The current price-availability disconnect suggests manufacturers are absorbing raw material cost increases. This cannot continue indefinitely. Either finished component pricing will increase to reflect tantalum ore inflation, or manufacturers will curtail production, extending lead times significantly. The stability of 16-18-week lead times despite 110% ore price increases indicates manufacturers are prioritizing market share over near-term margins—a strategy that has historical precedent but finite duration.

4. Long-term supply agreements become increasingly valuable in this environment. Organizations with committed volume agreements at negotiated pricing insulate themselves from both spot market volatility and capacity allocation uncertainties. The premium paid for supply security during stable periods justifies avoiding 30+ week lead times and emergency expedite fees during crisis conditions.

5. Design flexibility and alternative component qualification should be ongoing initiatives. While tantalum capacitors offer unique performance characteristics, applications with some specification flexibility should maintain qualified alternatives. MLCC technology continues advancing, polymer capacitors serve certain low-ESR applications and aluminum electrolytics remain viable for larger case sizes. Proactive qualification efforts during periods of stable availability prevent reactive scrambling during shortages.

OUTLOOK AND STRATEGIC RECOMMENDATIONS

The tantalum capacitor market stands at a critical juncture characterized by fundamental contradictions that will resolve over the next 12-18 months. Tantalum ore prices have surged 110% while capacitor lead times remain relatively stable. Global EV production accelerates even as the U.S. market moderates. AI infrastructure emerges as a major demand vector just as traditional applications face economic headwinds.

Our analysis of 165 months of ore pricing data and 132 months of lead time tracking provides several high-confidence conclusions:

The price-availability disconnect is temporary, not sustainable. Historical patterns demonstrate that manufacturers cannot indefinitely absorb raw material cost inflation without either raising finished component prices or curtailing production. The current stability reflects strategic positioning and healthy margins, but economic pressure will eventually transmit to end customers through either pricing or availability constraints.

Lead times will likely continue to gradually extend through 2026-2027. We expect lead times to reach the 20-24-week range by late 2026, representing elevated but manageable conditions. Barring major supply disruptions or unexpected demand shocks, we anticipate slow-motion tightening rather than an acute crisis. However, organizations must plan for this trajectory and secure positions accordingly.

The AI-EV capacity allocation question will intensify. As AI infrastructure buildout accelerates and manufacturers allocate limited production capacity, traditional applications may find themselves competing for priority. The narrative that AI is 'absorbing capacity freed by falling U.S. EV demand' oversimplifies global dynamics but captures real competitive pressure for manufacturing resources.

Proactive supply chain management becomes a competitive necessity. The volatility documented in our historical data series—from an eight-week baseline to 43-week crisis peaks—demonstrates that reactive approaches fail during shortage periods. Organizations must develop sophisticated demand forecasting, maintain long-term supplier relationships, build inventory buffers during stable periods and pursue design flexibility initiatives before constraints emerge.

The tantalum capacitor market has navigated extraordinary turbulence over the past decade while remaining essential to modern electronics. From conflict minerals compliance through pandemic disruptions to the current AI-driven demand transformation, supply chains have demonstrated remarkable resilience. However, resilience should not be mistaken for invulnerability.

Organizations that internalize the lessons from 165 months of ore price volatility and 132 months of lead time tracking will position themselves advantageously for whatever challenges emerge. Those who assume current stability represents permanent equilibrium risk finding themselves unprepared when the inevitable next inflection point arrives.

Dennis M. Zogbi is CEO and Founder of Paumanok Publications, Inc., a research and consulting firm specializing in passive electronic components markets. Paumanok has maintained continuous tracking of tantalum capacitor lead times, pricing, and market dynamics for over three decades, providing critical market intelligence to manufacturers, distributors, and OEM procurement organizations worldwide.

Follow TTI, Inc. on LinkedIn for more news and market insights.

Statements of fact and opinions expressed in posts by contributors are the responsibility of the authors alone and do not imply an opinion of the officers or the representatives of TTI, Inc. or the TTI Family of Specialists.

Follow TTI, Inc. - Europe on LinkedIn for more news and market insights.

Statements of fact and opinions expressed in posts by contributors are the responsibility of the authors alone and do not imply an opinion of the officers or the representatives of TTI, Inc. or the TTI Family of Specialists.